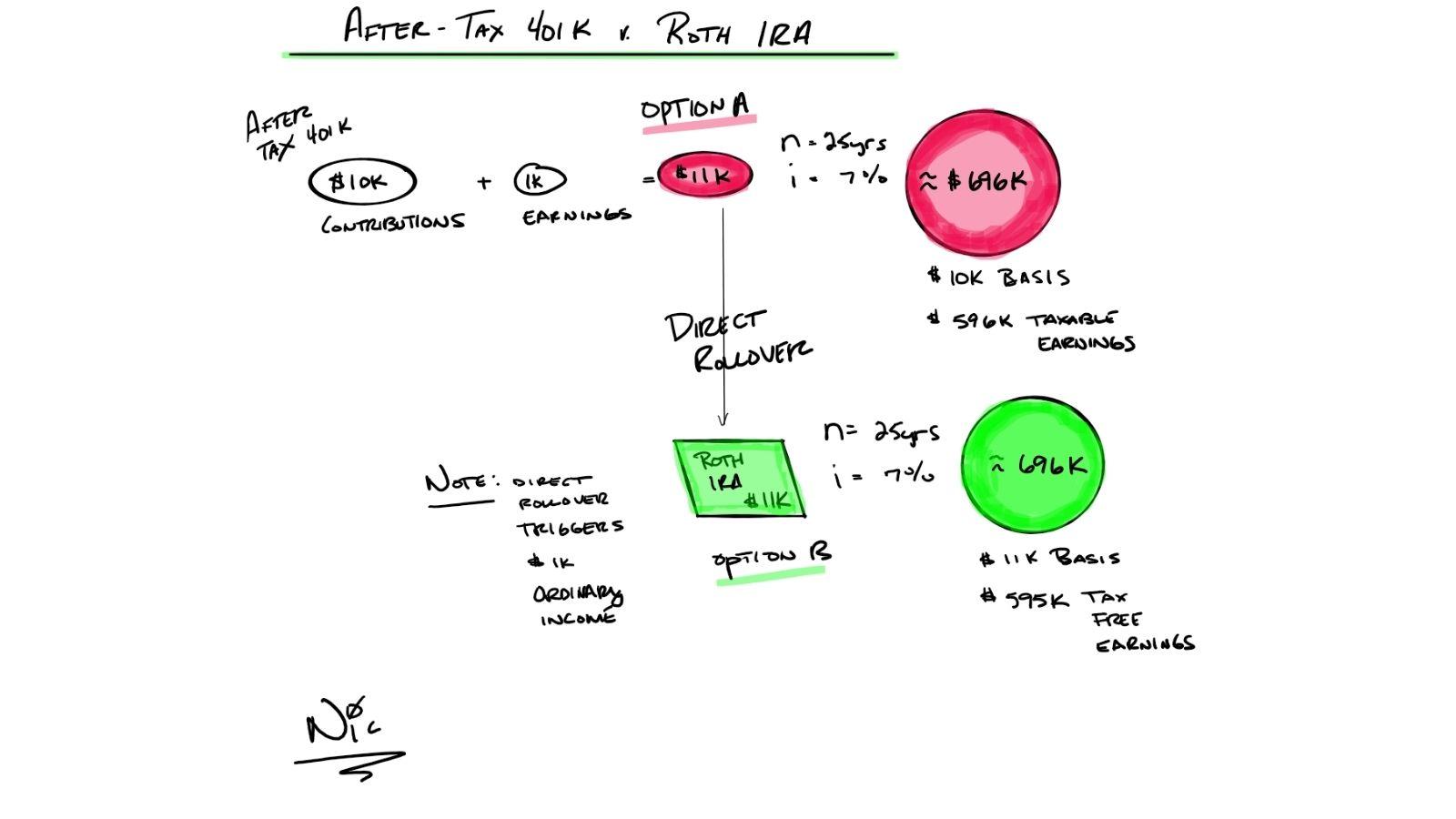

Be careful of accumulating funds in an after-tax 401k IF you can facilitate a “direct rollover” to a Roth IRA. Consider this example:

This year, you contribute $10k to an “After-Tax 401k” and it grows to $11k at the end of the year. At the end of the year, you might be able to roll these funds into a “Roth IRA.”

- Option A: Leave the funds in the After-Tax 401k. Let’s assume over the next 25 years the funds grow by 7%. At the end of 25 years, the account has grown to approximately $696k. During retirement, approximately 98.5% would be taxed at ordinary income.

- Option B: Direct Rollover to a Roth IRA. You would realize $1k of ordinary income. However, during retirement, 100% of the funds could be withdrawn tax-free (assuming you are 59 ½ years old and the Roth IRA has been open for at least 5 years).

IMPORTANT INFORMATION

Information in this material is for general information only and not intended as investment, tax, or legal advice. Please consult the appropriate professionals for specific information regarding your individual situation prior to making any financial decision.

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing. Unqualified Roth IRA withdrawals may result in a 10% IRS penalty tax.